For many UK expats, investing in property back home can feel like a “no-brainer”. It’s familiar and the tangible nature of bricks and mortar can feel more reassuring than the lesser-known world of stocks and shares.

Historically, property has offered the opportunity for both rental income and long-term capital growth. Along with favourable tax treatment, rising house prices, and strong demand, buy-to-let has long been an attractive proposition.

However, recent tax reforms, higher Stamp Duty charges, and new regulations for landlords mean that investing in property is no longer the no-brainer it once was.

If you own buy-to-let property in the UK or are thinking about buying a UK rental property while living abroad, read on to understand more about how these changes could affect you and your potential returns.

The property tax landscape is changing

If you’re living overseas but investing in UK buy-to-let property, there are several taxes that could affect your overall return.

Income Tax on rental income

Rental profits from UK property are typically subject to Income Tax at your marginal rate, even if you live overseas.

While certain small allowances exist – such as the £1,000 Property Allowance – most landlords will pay tax on their rental profits after deducting allowable expenses.

Before 2017, you could deduct mortgage interest and other finance costs such as mortgage arrangement fees from your rental income, but now you receive a 20% tax credit.

If you’re a higher-rate taxpayer and used to receive 40% tax relief on mortgage payments, this could make a significant dent in your profits.

And there’s another upcoming change: from April 2027, the rate of tax on property income will increase by 2% across all tax bands to 22%, 42%, and 47% respectively.

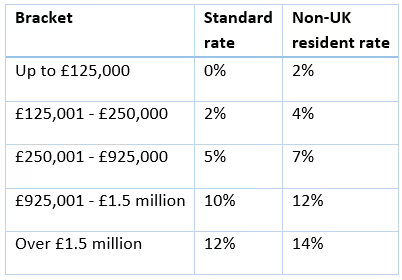

Stamp duty surcharges for overseas buyers

Thanks to Stamp Duty, the initial tax bill could be far higher than you might anticipate.

Here’s a breakdown of the current Stamp Duty Land Tax (SDLT) rates:

Unless you spend at least 183 days (6 months) during the 12 months before you purchase your property, you’ll be deemed “not a UK resident” and charged the higher rate of SDLT.

Depending on your circumstances, you could face three layers of SDLT:

- The standard SDLT rate on the property purchase.

- A 5% surcharge for buying an additional residential property.

- A 2% surcharge applied to non-UK residents.

These additional charges could add thousands of pounds to the upfront cost of buying a rental property, so it may be worth running through all the calculations to make sure investing in property is still the smartest choice.

Capital Gains Tax when you sell

When you eventually sell an investment property, Capital Gains Tax (CGT) may apply to any profit you make.

For the 2025/26 tax year, gains on residential property are typically taxed at:

- 18% for gains within the basic-rate band

- 24% for gains above the basic-rate band.

That said, even UK expats have a £3,000 annual CGT allowance (2025/26 and 2026/27), which you could use to help reduce your taxable gain.

New tenant protections could reshape the rental market

Alongside tax changes, the UK rental market is also undergoing one of its biggest regulatory overhauls in decades.

From May 2026, new legislation will introduce stronger rights and protections for tenants in England.

Some of these changes may alter the way you manage your rental property.

For example, one of the most significant reforms is the abolition of “no-fault” evictions, meaning you’ll no longer be able to ask tenants to leave without a valid legal reason.

Meanwhile, fixed-term tenancies will be replaced by rolling contracts, giving tenants greater flexibility to leave with two months’ notice.

The new rules will also:

- Limit how you manage rent and tenant selection

- Restrict rent increases to once per year

- Prevent bidding wars as landlords must advertise and charge the same rent.

These changes may mean it becomes more time-consuming and effortful to manage your UK rental property.

While property may still play a role in your portfolio, it shouldn’t be your only investment

Despite tax and regulatory changes, buy-to-let property can still form part of a long-term investment strategy.

The MSCI World Index tracks equity markets across developed countries and is a useful benchmark for global stock market performance.

Over the 20 years to 2021, global equities delivered an average return of 149%, marginally ahead of UK residential property at 147%.

But the difference becomes far more noticeable when you look at more recent data: between 2011 and 2021, global equities returned 134%, compared with 58% for UK property.

The key takeaway is that property may still have a place in your long-term financial plan, but it may no longer represent the simple investment opportunity you previously enjoyed.