Your life expectancy will play a key role when it comes to your financial plan. But your lifespan isn’t the only thing you should be considering.

To ensure you’ve thought about every eventuality, you also need to think about your realistic health span, and how long your wealth will last.

In short, the three spans that will play a role in your financial plan are your lifespan, health span, and wealth span.

Let’s break things down.

Understanding your expected lifespan can help you plan a sustainable income

Your longevity is an important aspect of your long-term financial plan.

Your expected length of life may be impacted by social, economic, behavioural, and biological factors over the course of your life.

If you’re not sure where to start, look back at your ancestors. How long your parents, grandparents, and great grandparents survived could indicate how long you might expect to live.

Thinking about your expected lifespan will help you to understand how long your wealth will need to last once you retire. As well as ensuring you have a sustainable income, it can also give clues about the legacy you may leave.

To ensure that your wealth will last your lifetime, your financial plan may use a range of tax-efficient strategies.

According to the Office for National Statistics (ONS) in the UK 65-year-old males have an average life expectancy of 85, and a 1 in 4 chance of living to 92. 65-year-old females fare better, with an average life expectancy of 88, and a 1 in 4 chance of living to 94.

Meanwhile, data from Statista reveals that the average global life expectancy has risen from around 46 in 1950 to around 73 as of 2023. Continuing at the current rate, projections suggest that the average global life expectancy could be over 81 by the end of the century.

The longer your health span, the more time you’ll have to enjoy life in good health

Your health span is the period of time you spend in good health, free from chronic diseases and other issues that arise with age.

While your health span is often dictated by your family’s medical history, your lifestyle choices may also make a significant difference.

As could where in the world you live.

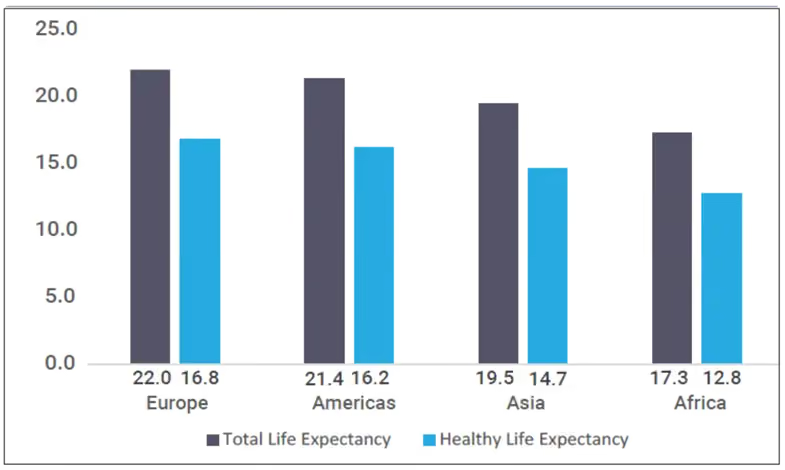

The chart below compares the total life expectation with the number of years of healthy life expectancy, as of 2019.

Source: Economist Impact based on data from WHO Global Health

Though average life expectancy and healthy life expectancy have both increased over recent years, healthy life expectancy is increasing more slowly.

In fact, as the chart shows, you could spend five years of life in poor health. Since these figures are taken from 2019, it’s feasible that more people may well suffer ill health for far longer in future. Particularly when you consider the ongoing pharmaceutical and medical advances being made.

Another area that’s slowly gaining ground, and may be worth your attention, is functional health. Rather than relying on conventional healthcare, functional practitioners identify the root cause of health issues, and take a holistic approach.

Focusing on your dietary choices, exercise and mindset, alongside a personalised range of vitamins and supplements, could help you to enjoy greater wellbeing, not to mention a longer health span.

Download your free guide: Planning for a longer life: Wellbeing tips and financial management strategies

Increasing the number of years you can enjoy feeling vibrant and healthy can also allow you more time and money to do what makes you happy.

In short, the more years you’re able to remain in good health, the less time you’ll spend in hospitals or visiting doctors. Plus, you’ll save money that you might otherwise have spent on potentially costly treatment.

Your lifespan and health span will have a direct effect on your wealth span

Your wealth span will depend how you adapt your current and future wealth management in light of increased life expectancy.

When thinking about your financial plan, it’s sensible to take flexible approach, allowing for both good health and the possible need for care.

The cost of care will depend on where you live. To give you an idea, in the UK, according to figures from the NHS, on average in 2025/26 in England you’d expect to pay:

- £20 an hour for home care

- £700 a week for residential care

- £850 a week for nursing care

- £800 – £1,600 a week for a live-in carer.

Using cashflow planning, a financial planner could give you peace of mind over your wealth span.

We regularly use this tool to help clients visualise their wealth. The clever financial software can help you accurately model your spending and how this might affect your future wealth.

Inputting data about the wealth you already own – the value of your investments, property, and any cash savings you might have – we then account for your monthly income and expenditure.

From here, we can build an accurate forecast of how your finances are likely to change over time, helping your visualise how long your wealth will last and if you have adequate funds to achieve your goals.

In the event that the data shows a potential shortfall, we’ll help you adjust your financial plan and advise on options to build more savings.

If you’d like to discuss your financial plan and ensure it adequately accounts for your life, health, and wealth spans, we’d be delighted to hear from you.