Life is all about balance, and that is especially true when it comes to withdrawing a sustainable income from your retirement savings.

After working hard and saving for many years, when you come to retire you are likely to be excited to spend some of your savings on fulfilling your ambitions. But it can be tricky to be sure how much you can withdraw and spend today without negatively affecting your financial security in the later years of your retirement.

The rising cost of living as well as the potential cost of later-life care must all be considered when deciding how much of your pension savings to spend each year. While there are some rules of thumb that have been used in the past, few are likely to be accurate enough to suit your specific circumstances.

Read on to learn more about how your financial planner can help you to calculate a suitable withdrawal rate so that you can enjoy your retirement today without risking future financial problems.

In the past, the “4% rule” provided some guidance about how much to withdraw from your pension

To help retirees calculate how much they can withdraw from their pension to maintain their preferred lifestyle throughout retirement, in 1994, American financial planner William Bengen suggested the “4% rule”.

This rule of thumb suggests that retirees withdraw 4% of their total pension pot in the first year of their retirement. Then, in each subsequent year, they can withdraw the same value adjusting for inflation.

According to Bengen, this would enable the pension to last throughout a 30-year retirement. In fact, Professional Adviser reports that he later clarified that 4% was a worst-case scenario, and the actual optimal withdrawal rate may be closer to 7% or even 13% depending on market conditions.

The 4% rule may not be suitable for everyone

In recent years, financial experts have suggested that the 4% rule may not be sustainable for the majority of people. There are several reasons for this:

1. Your retirement expenses may fluctuate from year to year

The 4% rule assumes that your expenditure will remain consistent throughout your retirement, accounting only for changes in the cost of living. But this doesn’t reflect the reality for many people.

In the early years of your retirement, you may have higher expenses as you make the most of your new free time achieving your lifetime goals. Maybe you’d like to renovate your house, travel the world, or pursue new hobbies while you still have the energy and stamina.

After you have achieved these goals, or if your health starts to decline, your expenses may fall as you feel more content to stay at home. Then, many people are likely to need help in their later years with healthcare or daily tasks such as cooking or cleaning. So, these needs could cause your expenses to rise again.

Your retirement income strategy needs to factor in each of these three stages of retirement for it to be truly sustainable for you.

2. Your pension fund can fall in value as well as rise

One of the problems with the 4% rule is that it assumes a certain level of investment growth on the savings you keep invested in your pension. But Bengen based these calculations on US investment data, so depending on how your pension is invested, this may not be applicable.

Additionally, the nature of investing in the stock market means that your savings can fall in value as well as rise. You may need to adjust your withdrawal rate if your pension savings or investments experience a short-term dip in value.

3. Withdrawing more than you need means your savings could lose spending power

If your expenses require a lower withdrawal rate than 4%, taking out more than you need could be risky. Cash savings accounts rarely offer interest rates that keep pace with inflation, so holding more of your wealth in cash than is necessary could reduce your buying power over time.

By comparison, keeping your wealth invested could offer you more opportunities to generate positive returns that help your portfolio to outpace inflation.

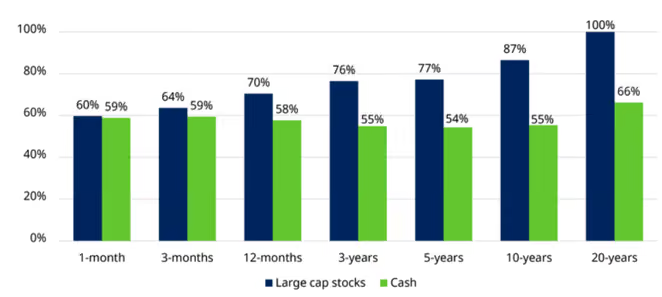

In the graph below, you can see the percentage of time periods in which stocks and cash have beaten inflation between 1926 and 2022.

This shows that cash beats inflation around 50% to 60% of the time but over any 20-year period, investing beats inflation 100% of the time.

Source: Schroders

So, it’s important to only withdraw what you need each year and be sensible about where you hold your savings and investments to avoid your money from losing buying power.

Your financial planner can help you to create a retirement income strategy that works for you

While it’s important to plan for your future, you also deserve to enjoy yourself today. That’s why it is sensible to consult a financial planner for guidance about how you can use your retirement savings.

They can create a cashflow forecast that enables you to see how much income you may need each year in your retirement. By entering data about your existing assets and liabilities, income, expenses, and key dates such as your retirement date, they can create an illustration of your income needs and net worth over time.

This can help you to identify a suitable withdrawal rate that will enable you to fulfil your ambitions while also providing peace of mind that you will be able to maintain your preferred lifestyle in the later years of your retirement.

Using this information, you can plan an effective retirement income strategy. It could also help you to create an estate plan, allowing you to leave a meaningful legacy to your loved ones after you’re gone without it affecting your financial wellbeing in the meantime.

Your planner will meet with you at regular intervals to check that your income strategy is still appropriate. They can also make any necessary tweaks if your circumstances or external factors have changed.